- Several major international pipelines are facing geopolitical risks in 2025, threatening the stability of global energy supplies and prices.

- Pipelines like the CPC and Druzhba are particularly vulnerable due to political tensions and potential disruptions that could affect millions of barrels of oil per day.

- The future of pipelines such as Nord Stream and EastMed remain uncertain, contributing to ongoing energy anxiety and shifts in European energy strategy.

In today’s high-stakes energy landscape, pipelines are more than conduits—they are critical geopolitical tripwires. These steel lifelines carry the hydrocarbons that power global economies, and many run through the most politically volatile regions on Earth. As energy markets tighten and global rivalries sharpen, the vulnerability of these routes transforms them into strategic flashpoints.

From the Russian steppe to the Sahel, from Kurdish oil routes to frozen Nordic seafloors, infrastructure once seen as fixed and dependable is now anything but. Each of these pipelines represents a convergence of commercial interest and national security. Disruption in any form–economics, politics or conflict–will immediately jolt markets and recalibrate diplomatic alignments.

These seven pipelines, forming the front lines of today’s energy geopolitics, aren’t just energy assets. They are strategic pressure points whose fate could help determine tomorrow’s prices, alliances, and risks. If you’re watching energy markets in 2025, these seven deserve your closest attention.

#1 Caspian Pipeline Consortium (CPC)

Few pipelines shoulder as much geopolitical baggage as the CPC. Transporting up to 1.3 million barrels of Kazakh crude per day from the Tengiz field to Russia’s Black Sea port of Novorossiysk, CPC accounts for the bulk of Kazakhstan’s oil exports.

It’s not just about volume—the pipeline passes through Russian territory, placing it under indirect influence of Moscow’s shifting political posture toward the West. Any friction, from sanctions fallout to maritime conflict, could shut it down.

In 2022, weather and technical snags cut CPC flows, causing a brief but sharp spike in prices. A future political disruption would be even more dramatic. For markets already teetering on tight supply-demand margins, a CPC shutdown would be a gut punch. This disruption contributed to Brent crude prices surging by over 5%, reaching approximately $121.60 per barrel. The price spike occurred over a short period, reflecting market concerns about the loss of a critical supply route that handles about 1.2 million barrels per day, or roughly 1.2% of global oil demand.

In May 2025, CPC exports were projected to fall significantly—down to 4.5 million metric tons from 5.3 million in April—due to maintenance and port capacity limits at Novorossiysk. Compounding matters, a Russian court recently ruled to keep CPC’s export infrastructure operational despite environmental permit disputes, suggesting that Moscow continues to use the pipeline as geopolitical leverage. The ruling prevented a possible shutdown that could have slashed deliveries by hundreds of thousands of barrels per day. Related: Trump to Use Emergency Powers to Boost U.S. Critical Minerals Industry

While flows continue, these episodes have underscored the fragility of the CPC route. With Russia asserting greater regulatory control and Kazakhstan’s reliance growing, any serious disruption would strip global markets of a major light crude source, triggering immediate price volatility.

#2 Druzhba Pipeline

Europe’s largest and longest crude oil pipeline, the Druzhba (“Friendship”) line, once symbolized post-war cooperation. Today, it’s a geopolitical flashpoint. Spanning over 4,000 kilometers, Druzhba delivers Russian Urals crude to Central and Eastern Europe, including Poland, Hungary, Slovakia, and the Czech Republic.

Before Russia’s full-scale invasion of Ukraine, the pipeline moved over 1 million bpd. Those flows have since diminished, but several landlocked European nations remain dependent. The Druzhba pipeline, once a cornerstone of Russian oil exports to Europe, has experienced a significant decline in throughput since the onset of the Russia-Ukraine conflict in 2022. Prior to the conflict, the pipeline transported approximately 800,000 barrels per day (bpd) of crude oil. As of early 2025, this volume has decreased to just under 280,000 bpd, marking a reduction of over 65%, according to Energy Intel.

This substantial decrease is attributed to a combination of factors, including European Union sanctions, diversification efforts by member states, and geopolitical tensions. Countries like Germany and Poland have ceased imports via the Druzhba pipeline, while others, such as the Czech Republic, have invested in alternative infrastructure like the Transalpine Pipeline (TAL) to reduce dependence on Russian oil. Despite these reductions, certain landlocked nations, notably Hungary and Slovakia, remain reliant on the Druzhba pipeline due to limited access to alternative supply routes.

Geopolitically, Druzhba is a symbol of energy leverage. Ukraine controls a key section of the pipeline and has used transit fees to pressure Moscow. In early 2023 and again in late 2024, oil flows through the southern branch were disrupted due to unpaid transit fees and damage allegedly tied to sabotage and war-related instability. The northern branch to Poland and Germany was largely halted in 2022, as both countries pivoted away from Russian oil.

U.S. sanctions have added a second layer of complexity. Recent moves to target financial intermediaries facilitating Russian energy exports could restrict payment mechanisms for pipeline shipments. Though the EU has allowed some exemptions to maintain supplies to Hungary and Slovakia, Washington’s tightening enforcement may eventually force Europe to phase out Druzhba altogether.

Technically, the pipeline remains functional but increasingly fragile. Ukrainian officials have warned that continued Russian strikes near critical infrastructure—coupled with aging Soviet-era hardware—raise the risk of prolonged outages.

If Druzhba were fully shut down, countries like Hungary would be forced to secure alternative supplies via the Adria pipeline from Croatia, which lacks sufficient capacity for a smooth transition. The result would be higher transportation costs, disrupted refinery operations, and renewed political friction within the EU.

#3 Kirkuk–Ceyhan Oil Pipeline

The Kirkuk–Ceyhan pipeline links Iraq’s northern oilfields to the Turkish port of Ceyhan, with a theoretical capacity of 1.6 million barrels per day (bpd). However, due to political and legal disputes, actual throughput has been well under 400,000 bpd. This pipeline is Iraq’s primary export route for crude from the semi-autonomous Kurdistan Region, making it both an economic and geopolitical lifeline.

In March 2023, flows were halted after an international arbitration court ruled in favor of Baghdad, stating Turkey violated previous agreements by allowing oil exports from the Kurdish region without Iraq’s federal approval. Since then, tensions between Baghdad and Erbil have intensified exponentially. Efforts to resume flows have repeatedly stalled over unresolved revenue-sharing mechanisms and export rights.

The situation has grown more complex in 2025. The Kurdish Regional Government (KRG) has independently signed multibillion-dollar energy deals with U.S. firms, prompting Baghdad to accuse Washington of violating Iraq’s sovereignty. Baghdad filed a lawsuit against the U.S. in international courts, claiming that these direct agreements infringe on Iraq’s constitution, which vests control of oil exports with the federal government.

This dispute has exposed fault lines not only within Iraq but also in its international relations. Washington’s implicit backing of the Kurdish contracts has drawn backlash in Baghdad and Tehran, further politicizing the pipeline’s future. Analysts warn that U.S. intervention risks destabilizing efforts to resolve Iraq’s long-standing oil governance crisis, while delaying a restart of the Ceyhan route.

If flows remain shuttered, the economic blow to the KRG—already reliant on oil for nearly 90% of its revenue—could be severe. For Mediterranean crude markets, the loss of this medium sour grade continues to tighten regional supply and complicate sourcing strategies for refiners.

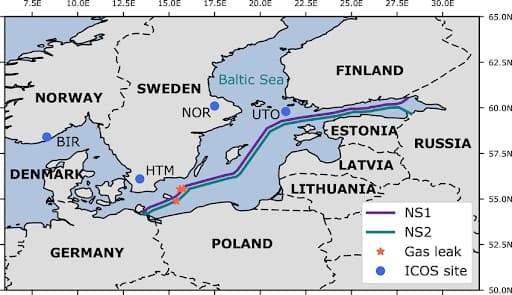

#4 Nord Stream 1 & 2

Though offline since its 2022 sabotage, Nord Stream 1 still casts a long shadow over European energy policy. Before its abrupt halt, it delivered 55 billion cubic meters of Russian gas annually to Germany—making it a central artery of the continent’s energy infrastructure. Its shutdown catalyzed a transformation in European energy strategy, spurring a surge in LNG terminal construction and a recalibration of foreign energy dependencies.

If Russia or Germany even floated reactivation talks, gas prices would jolt upward. The pipeline, though inactive, remains the fulcrum of Europe’s energy anxiety.

In 2025, Russia officially confirmed the permanent halt of all gas flows through the pipeline, closing the chapter on one of the world’s most significant energy corridors. Despite this, debate over its future remains contentious.

Germany’s economy minister recently vowed to oppose any revival efforts, framing the pipeline as a strategic liability. In contrast, industry figures like TotalEnergies CEO Patrick Pouyanné have suggested that a return of Nord Stream gas “cannot be ruled out,” reflecting lingering divisions within Europe’s energy establishment.

Nord Stream 2, the politically fraught twin pipeline completed but never operational due to regulatory blocks and Russia’s invasion of Ukraine, has also become a geopolitical symbol. Although physically intact, it remains idle, with no official plans to activate. Nevertheless, any mention of Nord Stream 2 in diplomatic circles tends to trigger immediate reactions across energy markets.

These pipelines remain geopolitically potent. Any signal of possible reactivation or renewed sabotage threats would likely jolt European gas prices. Even dormant, Nord Stream 1 and 2 serve as barometers of EU-Russia energy tensions and enduring symbols of Europe’s vulnerability and transition.

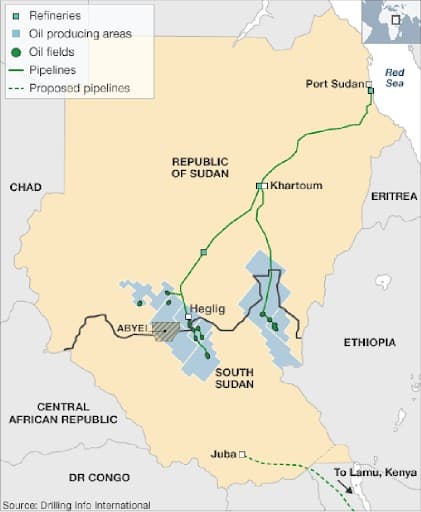

#5 Sudan–South Sudan Export Pipeline

South Sudan’s economy hinges on a single crude export lifeline: a 1,500-kilometer pipeline to Port Sudan. The conduit transports approximately 145,000 barrels per day—virtually the entirety of South Sudan’s oil exports—through volatile Sudanese territory. But Sudan’s ongoing civil war has rendered the route increasingly fragile.

In early 2024, clashes near Khartoum damaged sections of the pipeline, forcing Juba to declare force majeure and temporarily halt oil production. While flows resumed in mid-2025 following partial repairs, the risk of renewed disruption remains high. Sudan’s transitional government recently signaled its intent to suspend pipeline operations again, citing security concerns and political leverage. This is a dangerous escalation for South Sudan, whose budget depends on oil for over 90% of government revenues.

The instability in Sudan has also spilled over into South Sudanese politics.

Internal factions within the ruling SPLM-IG have used the pipeline crisis to attack rivals, aggravating existing tensions. Analysts warn that if oil revenues dry up, Juba could slide back into full-scale civil conflict. The UN Security Council’s recent extension of an arms embargo underscores fears that the region’s fragile peace is under threat.

Though small in global volume, the pipeline’s disruption would send ripples through heavy crude markets and exacerbate humanitarian crises in both Sudans. The infrastructure’s vulnerability—and its strategic centrality to South Sudan’s survival—make it a geopolitical fault line worth close scrutiny.

#6 Niger–Benin Export Pipeline

The Niger–Benin Export Pipeline is a new, high-stakes corridor aiming to transport up to 90,000 barrels per day of crude from Niger’s Agadem Basin to the Atlantic port of Sèmè in Benin. Backed heavily (at least it was) by China’s CNPC, the 2,000-kilometer pipeline is central to Niger’s ambitions of becoming a major West African oil exporter.

But political and security headwinds threaten the project’s stability. Just weeks after its inauguration, the pipeline came under attack by armed groups opposing Niger’s military junta, raising alarms about its operational future. The pipeline passes through regions plagued by jihadist violence and interethnic conflict, making it highly vulnerable.

Complicating matters further is a dramatic cooling of diplomatic ties between Niger and China. In April 2025, Niger abruptly cut ties with Beijing, accusing it of exploitative practices. Critics argue that CNPC’s dominance in Niger’s upstream and midstream oil sectors has left the country with limited economic control over its own resources. This rift raises questions about who ultimately benefits from the pipeline’s revenues and whether Beijing’s grip will loosen or harden.

Analysts note that any extended disruption would have limited global market effects due to the modest volumes involved. However, for Niger’s economy—where oil represents a crucial path to fiscal independence—the consequences would be profound. Moreover, any collapse of the project would be another geopolitical setback for China’s Belt and Road ambitions in Africa.

#7 EastMed Pipeline Dream

While not yet realized, the EastMed Pipeline has reemerged as one of the most geopolitically consequential energy infrastructure proposals in the world. The proposed pipeline would link offshore gas fields in Israel and Cyprus with Greece and potentially the broader European market, offering an alternative to Russian gas and bolstering Mediterranean energy integration.

Originally shelved due to cost and regional complexity, the EastMed revival in 2025 is driven by a convergence of strategic interests. A bipartisan U.S. bill introduced this year aims to integrate the EastMed pipeline into the India-Middle East-Europe Economic Corridor (IMEC), signaling strong transatlantic support.

At the same time, the UK and U.S. easing of sanctions on Syria to support Eastern Mediterranean development underscores the West’s broader pivot toward this route as a geopolitical counterbalance to both Russia and China.

However, the project remains mired in unresolved territorial and diplomatic disputes. Turkey continues to oppose the pipeline, claiming it bypasses its maritime jurisdiction and threatens Turkish Cypriot interests. Ankara’s military presence in Northern Cyprus and its growing ties with Libya compound the tension. Cyprus, as the geographic hub, has now become a geopolitical flashpoint, with EU, U.S., and UK actors all weighing in.

If built, EastMed could transport up to 10 bcm per year, significantly reshaping gas flows into Southern Europe. Its completion would dilute Russian energy leverage, strengthen Israeli-European ties, and potentially alter naval dynamics in the Eastern Mediterranean. On the other hand, delays or conflict escalation could destabilize the region further and leave Southern Europe energy-vulnerable.

By Tom Kool for Oilprice.com

More Top Reads From Oilprice.com

Tom Kool

Tom majored in International Business at Amsterdam’s Higher School of Economics, he is Oilprice.com’s Head of Operations